What are Perpetual Futures? How They Work and Why Traders Use Them

Perpetual futures are derivative contracts that let you go long or short on a crypto asset indefinitely, no settlement date, no rollover. Here's everything you need to understand before you trade.

If you've spent any time on a crypto trading platform, you've probably noticed that most of the volume isn't in spot markets. It's in perpetual futures. On any given day, perpetual futures across major venues trade at multiples of spot volume. And yet for many traders, how they actually work remains murky.

This guide breaks down what perpetual futures are, how the mechanics function under the hood, and what you need to understand before you open your first position. Whether you're coming from spot trading, traditional futures, or you're just starting to explore what are perps in crypto and why they dominate trading volume, this is the right starting point.

What "perpetual" actually means in trading

A perpetual futures contract is a derivative instrument that lets you speculate on the price of an asset, long or short, without ever having to take delivery of it or roll your position into a new contract. The defining feature is right there in the name: it has no expiry date.

Standard futures contracts (the kind traded on CME for commodities or equity indices) always have a settlement date. When that date arrives, the contract expires and you either take delivery of the underlying asset or settle in cash. If you want to maintain exposure, you have to "roll" into the next contract — which costs money and creates friction.

Perpetual futures remove that entirely. You can hold a position for hours, days, or months. There's no calendar forcing your hand.

The theoretical groundwork was laid by economist Robert Shiller, best known for Irrational Exuberance, who proposed the idea of perpetual futures as a way to create continuous, no-expiry exposure to an underlying asset. BitMEX took that concept and built the first working implementation in crypto, launching it in 2016. It's since become the dominant derivatives product in the space, and the terms perpetual futures and perpetual swaps are used interchangeably across the industry. They refer to the same thing.

How perpetual futures work

The no-expiry design creates an obvious problem: without a settlement date, what stops the perpetual futures price from drifting far away from the actual spot price of the underlying asset? The answer is the funding rate.

The funding rate mechanism

The funding rate is a periodic payment exchanged directly between traders holding long and short positions. It's the mechanism that keeps the perpetual price anchored to spot.

Here's how it works in practice:

- When the perpetual price is trading above spot, longs pay shorts. This creates a cost for buyers, which discourages buying pressure and pushes the price back toward spot.

- When the perpetual price is trading below spot, shorts pay longs. This discourages short sellers and pulls the price back up.

| Condition | Who pays | Effect |

|---|---|---|

| Perp price > spot price | Longs pay shorts | Reduces buying pressure, price moves toward spot |

| Perp price < spot price | Shorts pay longs | Reduces selling pressure, price moves toward spot |

| Perp price = spot price | No payment (or near zero) | Market is in equilibrium |

Funding is typically settled every 8 hours, though this varies by exchange. The rate itself is calculated based on the difference between the perpetual price and the spot index price, plus an interest rate component.

For longer-term position holders, funding rate costs accumulate and can significantly eat into returns — particularly in strongly trending markets where one side of the book consistently pays. This is one of the most underappreciated costs in crypto derivatives trading.

Leverage and margin

Perpetual futures are margined instruments — you don't pay the full notional value of a position upfront. Instead, you post a fraction of it as collateral (your margin), and the exchange provides the rest as leverage.

Two margin figures matter:

- Initial margin: The minimum collateral required to open a position. At 10x leverage, this is 10% of the notional value.

- Maintenance margin: The minimum collateral required to keep a position open. If your account equity falls below this threshold, your position is liquidated.

Liquidation happens automatically and immediately. There's no phone call, no grace period. When your margin is exhausted, the exchange closes your position — and depending on market conditions, slippage in the liquidation can push your loss beyond your initial margin if the exchange doesn't have adequate insurance fund coverage.

Use leverage with clear position sizing logic. The math is straightforward: a 10x leveraged position is liquidated if the price moves 10% against you (before fees). At 20x, that's 5%.

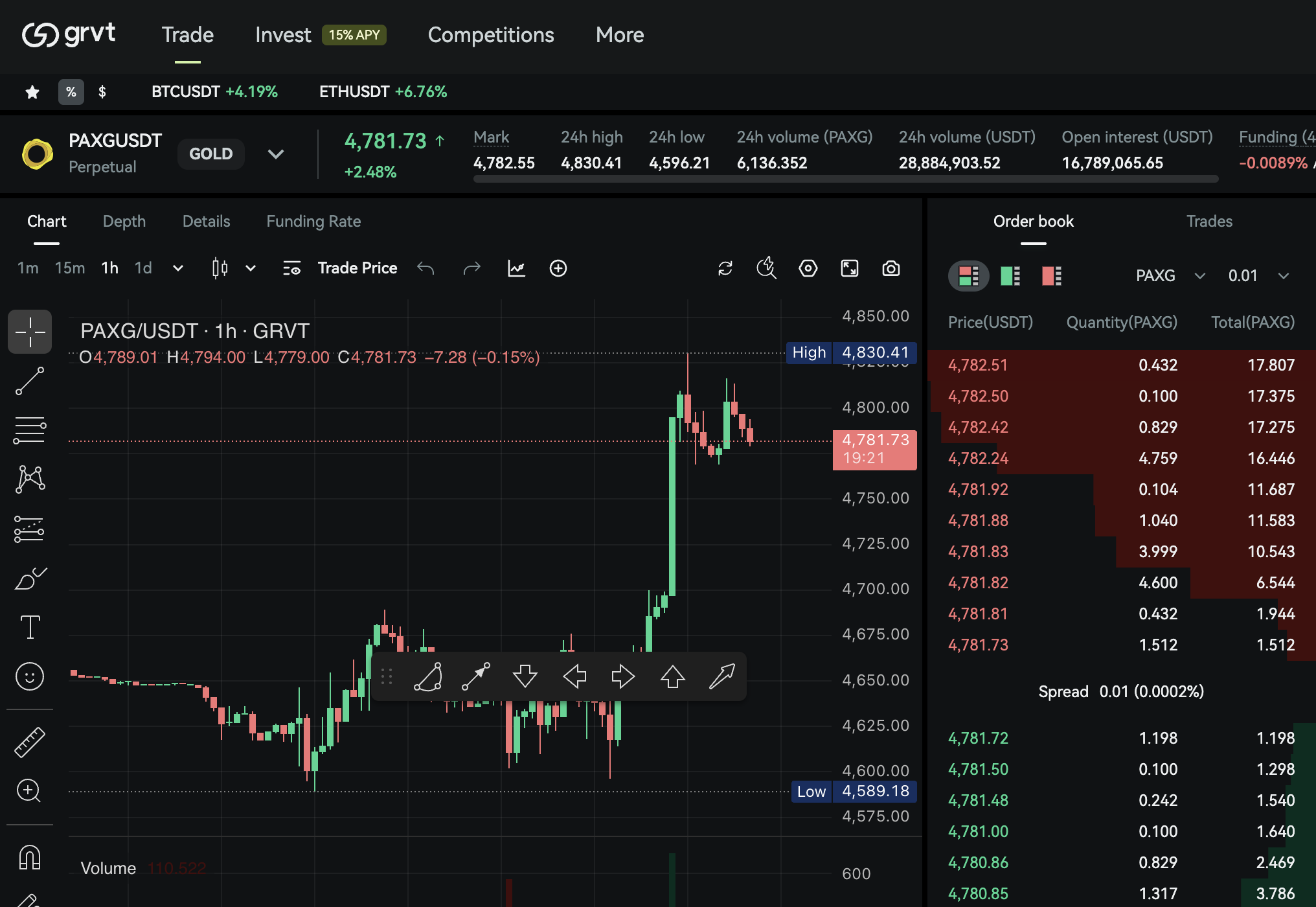

Mark price vs last price

Most exchanges, including Grvt, calculate liquidations based on mark price, not last traded price. Mark price is derived from spot index prices across multiple venues, dampened to prevent manipulation.

This distinction matters because last price can be temporarily moved by a large order or thin liquidity. If liquidations were triggered by last price, a single aggressive seller could cascade a wave of forced closures. Mark price prevents that.

Always check whether a platform uses mark price for liquidations before trading.

Perpetual futures vs standard futures contracts

The differences between perpetual futures and traditional dated futures are structural, not just cosmetic.

| Feature | Perpetual Futures | Standard Futures |

|---|---|---|

| Expiry date | None | Fixed (weekly, monthly, quarterly) |

| Settlement | No settlement | Cash or physical delivery at expiry |

| Price anchor | Funding rate | Convergence to spot at expiry |

| Rolling cost | Funding rate (ongoing) | Rollover cost at each expiry |

| Typical use | Short-to-medium term speculation | Hedging, longer-term positioning, institutional |

| Where traded | Primarily crypto native exchanges | CME, CBOE, traditional brokers |

For most crypto traders, perpetuals are the default choice. The lack of expiry removes operational complexity, and the continuous market structure suits the 24/7 nature of crypto markets. Dated futures contracts have their place, particularly for institutions that need specific settlement dates for hedging purposes, but for active speculation, perpetuals dominate.

What you can trade with perpetual futures

Bitcoin and Ethereum perpetuals are by far the most liquid markets, with deep order books across major venues and tight spreads even at size. These two markets alone account for the bulk of all crypto derivatives volume globally, and they're where most serious traders spend the majority of their time.

Beyond the majors, most large exchanges offer perpetuals on a range of altcoins, SOL, DOGE, AVAX, and dozens of others. Liquidity in altcoin perps is meaningfully thinner, which translates to wider bid-ask spreads, higher slippage on large orders, and greater vulnerability to price manipulation via the perp market itself. Funding rates can also become extreme in altcoin perps during periods of speculative excess, making them expensive to hold if you're on the crowded side.

For traders just starting out with perps, BTC and ETH are the right starting point, not because the opportunities are better, but because the market structure is more predictable and liquidation risk from thin liquidity is lower.

It's also worth noting how perpetuals fit into the broader derivatives landscape. Unlike options, which give you the right but not the obligation to buy or sell, a perpetual futures position is a binding obligation that marks to market in real time. Unlike spot trading, you don't hold the underlying asset — you hold a contract whose value is derived from it. That distinction matters for how you think about custody, counterparty risk, and what you actually own.

Trading perpetual futures on Grvt

Grvt is a hybrid decentralised exchange built on ZKSync, designed specifically for the demands of derivatives trading at institutional and professional-grade scale.

On the infrastructure side, Grvt operates an off-chain order matching engine, which means order execution speed is comparable to a centralised exchange.

Meanwhile, settlement is handled on-chain via ZKSync's zero-knowledge proof system. For traders who care about latency (algo traders, market makers, systematic strategies), this matters: you get CEX-level execution without custody risk.

Grvt's perpetual markets are built with API-first access in mind. If you're running a trading bot, a grid strategy, or any kind of programmatic execution, the Grvt API gives you the same depth and speed that institutional desks expect. The platform also offers granular margin controls and real-time position monitoring — the kind of tooling that makes risk management tractable rather than reactive.

This matters more than it might seem at first glance. Many traders move to perpetual futures because the instrument is powerful, then discover that the platform they chose wasn't built for serious use: slow APIs, opaque liquidation engines, poor mark price methodology. The infrastructure you trade on shapes your actual edge just as much as your strategy does.

Start trading perpetual futures on Grvt →

Key risks to understand before you trade

Perpetual futures are powerful instruments. They're also among the faster ways to lose money in crypto if the mechanics aren't respected. Three risks stand out.

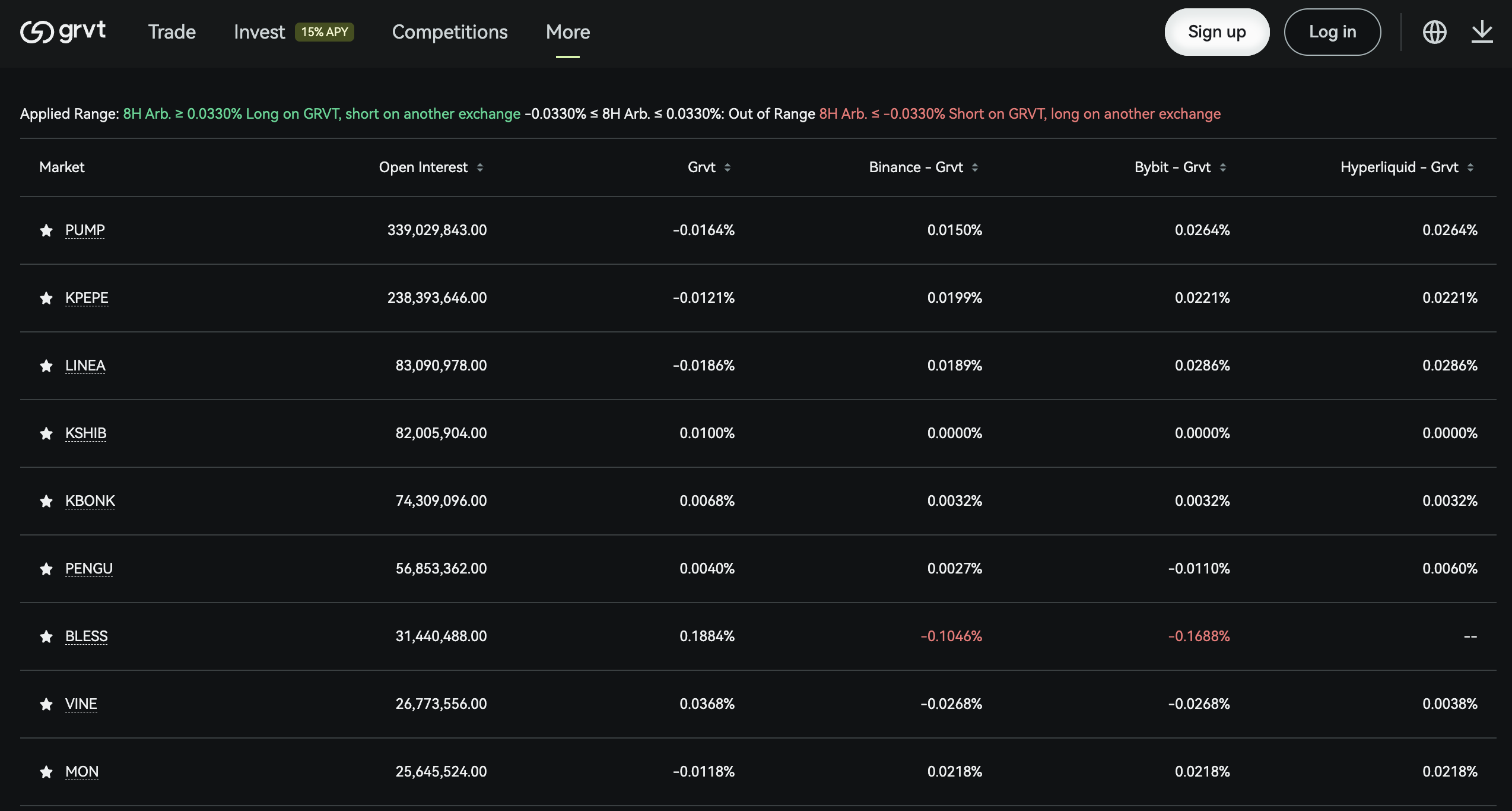

Liquidation cascades. In volatile markets, large liquidations can trigger a chain reaction. Forced selling pushes price down, which triggers more liquidations, which pushes price down further. If you're holding a leveraged long during one of these events, your position may be liquidated at a worse price than you'd expect from the initial move alone. Position sizing and stop losses are not optional. Monitoring open interest data alongside price action gives you early signals of when a cascade is building.

Funding rate exposure in trending markets. In a sustained bull run, longs consistently pay shorts. A position that's directionally correct can still lose money to cumulative funding costs over time, particularly at higher leverage. Check the current funding rate and annualise it before holding a position for more than a day or two. An annualised funding rate of 50%+ (which is not unusual during bull market peaks) means you're paying 50% per year just to stay in the trade. That's a high bar for directional return to clear.

Leverage amplifies in both directions. A 5x leveraged position that goes 10% in your favour doubles your margin. The same position going 10% against you wipes it out entirely. The asymmetry in perception, it doesn't feel like you're risking 100% of your capital, but you are, is what catches most new traders. Size positions as a percentage of total capital, not as a function of what the exchange will allow you to borrow.

Counterparty and platform risk. Unlike spot trading on a regulated exchange, you're trusting the platform's mark price methodology, insurance fund, and liquidation engine. A poorly designed platform can socialise losses across traders (auto-deleveraging), use a mark price that's easy to manipulate, or have an insurance fund too small to cover extreme moves. Understanding the mechanics of the specific platform you use is as important as understanding perpetual futures themselves.

Frequently asked questions

What is the difference between perpetual futures and futures contracts?

Standard futures contracts have a fixed expiry date and settle, either in cash or via physical delivery of the underlying asset, at that date. Perpetual futures have no expiry date and never settle. Instead, they use a funding rate mechanism to keep their price aligned with the spot market.

What does the funding rate mean in perpetual futures?

The funding rate is a periodic payment between traders on opposite sides of the market. When perpetual prices trade above spot, longs pay shorts (which pushes price back down). When perpetual prices trade below spot, shorts pay longs. It's the mechanism that keeps the perpetual price from diverging permanently from the real-world spot price.

Are perpetual futures the same as perpetual swaps?

Yes. The terms are used interchangeably across the industry. Both refer to the same instrument: a derivative contract with no expiry date, settled in crypto, using a funding rate to maintain price alignment with spot.

Can you hold a perpetual futures position forever?

Mechanically, yes. There's no expiry forcing you to close. In practice, the funding rate creates an ongoing cost if you're on the wrong side of the market sentiment, and margin requirements mean your position can be liquidated if the price moves against you enough. "Forever" is possible; it just requires active management of both funding costs and margin levels.

What is a good leverage ratio for perpetual futures?

There's no universal answer. It depends on your strategy, risk tolerance, and the volatility of the asset you're trading. A reasonable starting principle: use leverage low enough that a 15–20% adverse move doesn't liquidate your position. For most traders, that means 3–5x on major assets like BTC and ETH, and lower still on altcoins.

How to read funding rates as a market signal

Beyond their mechanical role, funding rates carry genuine information about market sentiment, and experienced traders use them as a signal in their own right.

When funding rates are persistently high and positive (longs paying shorts), it indicates the market is heavily long and leveraged. That's not necessarily a sell signal, but it's a warning that any negative price catalyst will be amplified by forced long liquidations. Conversely, sustained negative funding, shorts paying longs, suggests crowded short positioning and the potential for a sharp short squeeze.

Tracking the funding rate alongside price action, open interest, and spot market behaviour gives you a more complete picture of market structure than any single indicator. Many systematic traders build funding rate monitoring directly into their signal stacks, using it to calibrate position size or identify which direction has a structural tailwind from positioning dynamics.

An annualised funding rate of 50%+ (not unusual during bull market peaks) means you're paying 50% per year in carry costs just to hold a long. That's a high bar for directional return to clear, and it's the kind of number that makes holding positions overnight a materially different decision than opening them intraday.

Data on current and historical funding rates is available across most major perpetual exchanges and aggregators. If you're trading actively, building a habit of checking it before entering any position you plan to hold overnight is straightforward to implement and meaningfully reduces the chance of being caught offside by carry costs.

The bottom line

Perpetual futures are the dominant trading instrument in crypto derivatives for a reason: they're flexible, accessible, and structurally well-suited to a 24/7 market. But the funding rate mechanics, mark price calculations, and liquidation dynamics all require genuine understanding before you put capital at risk.

If you've read this far, you have the foundation. The next step is understanding how to size positions, read funding rate data as a market signal, and choose a platform that gives you the infrastructure to execute with precision.

Trade perpetual futures on Grvt →

Trading involves risk. This article is for informational purposes only and does not constitute financial advice.