Why Grvt Is Built Around Productive Capital

Grvt is built to be a capital productive DEX: idle trading margin earns up to 11% APY via the Yield Layer while your positions stay open. Independent research from Messari breaks down the mechanics and the growth behind it.

Messari, one of the most cited research firms in crypto, just published an in-depth report on Grvt. Here is what they found.

TL;DR

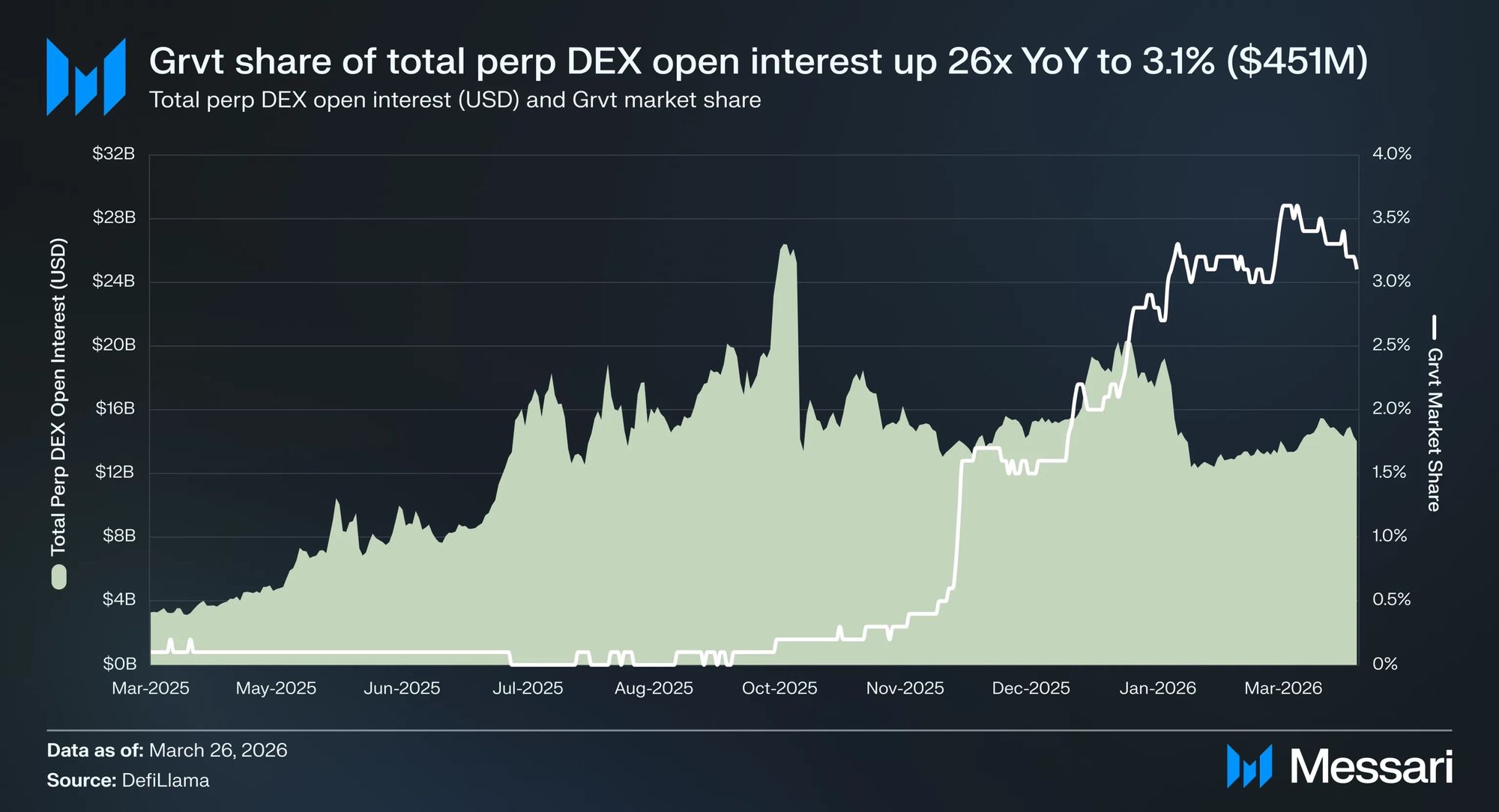

- Grvt's share of total perp DEX open interest grew 26x year over year, far outpacing the 4x growth of the broader market over the same period

- Unlike most perp DEXs where deposited collateral sits idle, Grvt routes it into real yield while your trades stay open, offering up to 11% APY on all collateral

- One-balance design is the structural reason this is possible: all collateral is treated as a single unified balance, enabling the Grvt Yield Layer to route idle capital into real yield via Aave while positions stay open

- Open interest is up 53% year to date to $451 million. TVL is up 36.8% to $80.4 million. Daily volume has ranged from $650 million to $2.6 billion in 2026

For the full picture, read the Messari report here: [Messari Report].

The rest of this article walks through the core mechanics behind those numbers.

Grvt's position in the perp DEX market

The perp DEX market is largely winner-take-most. Liquidity begets liquidity, and Hyperliquid currently leads with strong network effects. That makes Grvt's 26x increase in open interest market share year over year against a market that itself grew 4x, a meaningful signal. These are not numbers explained by one catalyst. They reflect a platform differentiated at the infrastructure level.

The separator: yield on margin

Yield on all collateral deposited to trade is what sets Grvt apart. The yield comes from two sources: a share of protocol trading fees, and rehypothecation of most user deposits to external DeFi protocols via Aave V3. Integrations with Morpho, Pendle, and Ethena are planned.

| Platform | Yield on collateral | Scope |

|---|---|---|

| Grvt | Up to 11% APY | All deposited collateral |

| Hyperliquid | Market rate on borrowable assets | Only assets not in use as collateral |

| Synthetix and similar | 2 to 11% APY via LSTs (e.g. sUSDe, wstETH) | Depends on the LST chosen |

On Grvt you do not choose between putting capital to work and using it to trade. The same balance does both. APY scales with trading activity across a four-week cycle, starting at 3.5% for five completed trades and reaching up to 11% at $5 million in volume. Maker fees are negative across all fee tiers, so climbing the APY ladder does not necessarily cost you fees to get there.

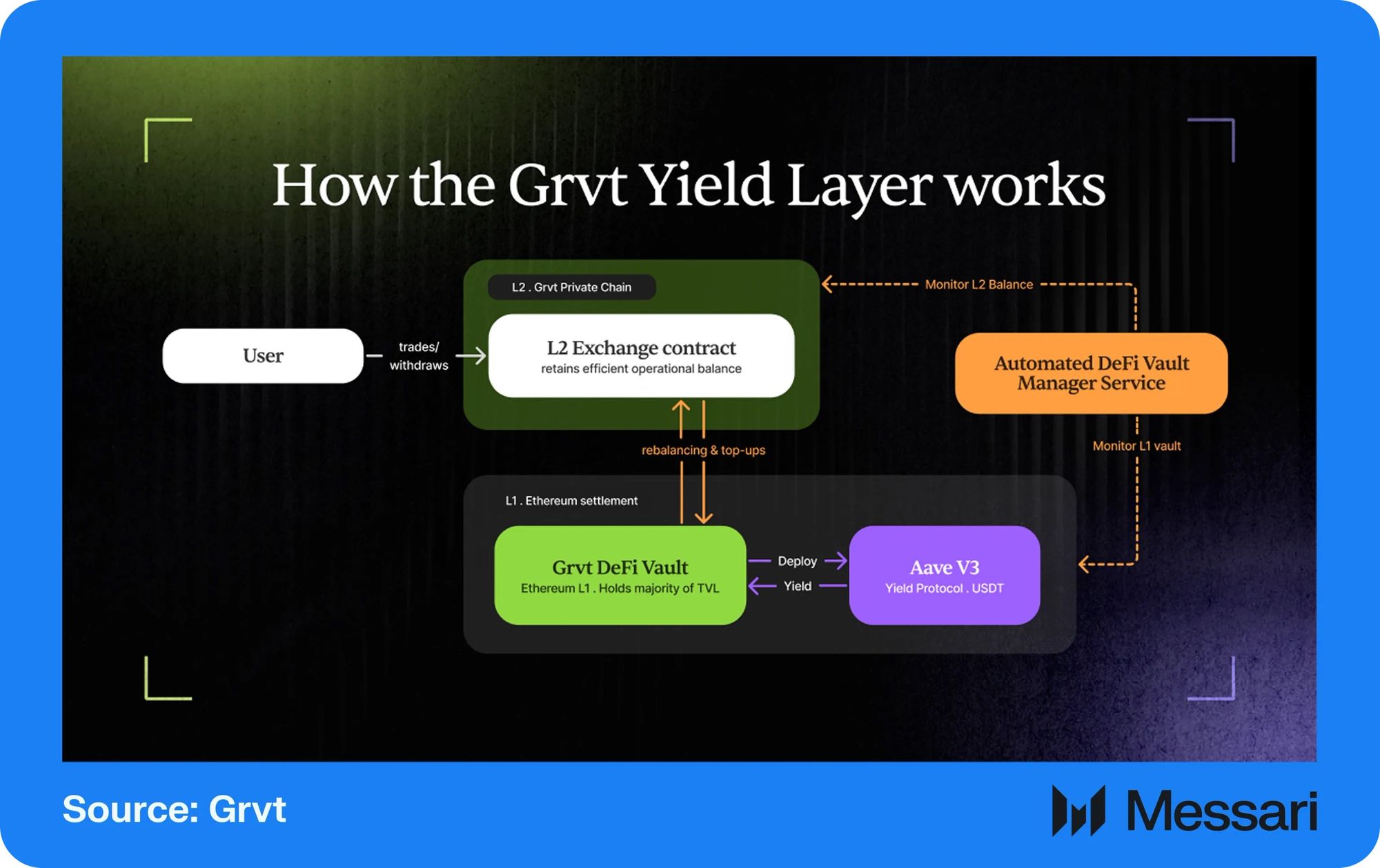

How one-balance design makes this possible

Yield on all collateral is structurally incompatible with isolated margin, where each position requires its own dedicated pool and capital cannot be redirected. Grvt operates on one-balance design: all collateral is treated as a single unified balance, simultaneously supporting all open positions and routing idle capital into yield strategies.

This is what the Grvt Yield Layer operationalizes. The same balance backing your trades is generating yield in Aave. That is only possible because the collateral is never locked per position. The risk tradeoff is real. Unified margin concentrates risk at the account level, which is why Grvt settles everything inside a ZK Validium system on ZKSync, ensuring correctness and privacy without publishing transaction data to Ethereum.

The Yield Layer as capital lifecycle infrastructure

Grvt decouples where collateral earns yield (Ethereum L1) from where activity is tracked (Grvt's private L2). Most deposits are rehypothecated to external DeFi protocols on L1, while the L2 retains enough for day-to-day withdrawals. The Aave integration is the first implementation of this design, proving that collateral deposited to trade can be composable with external DeFi without giving up the privacy guarantees of the Validium architecture.

Having built the trading infrastructure, the CLOB, ZK Validium settlement, and one-balance design, the Yield Layer is the next crucial step toward a full capital lifecycle system, where capital deposited to trade is also earning. Payments and spending come next, closing the loop so that capital never needs to leave the system to be useful. BTC, ETH, and yield-bearing RWAs as collateral extend that logic further, covering more of the capital lifecycle within a single self-custodial account.

The full Messari report covers the architecture, competitive landscape, and data in depth. Read it here: [Messari Report].

Ready to put your capital to work? Start trading on Grvt.